As the many fans of the HBO blockbuster show Succession know, managing transitions at family companies can be difficult — and entertaining. Another such drama is playing out in real life at Double Star, once a leading Chinese shoe brand.

According to Chinese media reports, in a letter to the staff last month, the company’s 84-year-old chairman, Wang Hai, accused his grandson of restricting his freedom for hours to force him to surrender the company.

Wang also alleged that his daughter-in-law and son — whom he had once described as “too lazy” to succeed him — broke into his office, assaulted staff and destroyed CCTV cameras, all in an effort to seize the company chop that is needed for critical documents. In China, he or she who controls the chop controls the company.

The fallout at Double Star highlights a common problem across China’s private sector: an entire generation of entrepreneurs who emerged in the 80s and 90s have either reached or are nearing retirement. Many are struggling to find a suitable heir.

“A lot of the second-generation either don’t have the capability to take over or they are not willing to take over,” says Oliver Rui, co-director of the Centre for Family Heritage at the China Europe International Business School in Shanghai. “That’s the current status.”

Many of them may not have prepared their children to become a leader, and not just individually, but also in terms of governance or the layout and structure of the company.

Kevin Au, director of the Centre for Family Business at Chinese University of Hong Kong

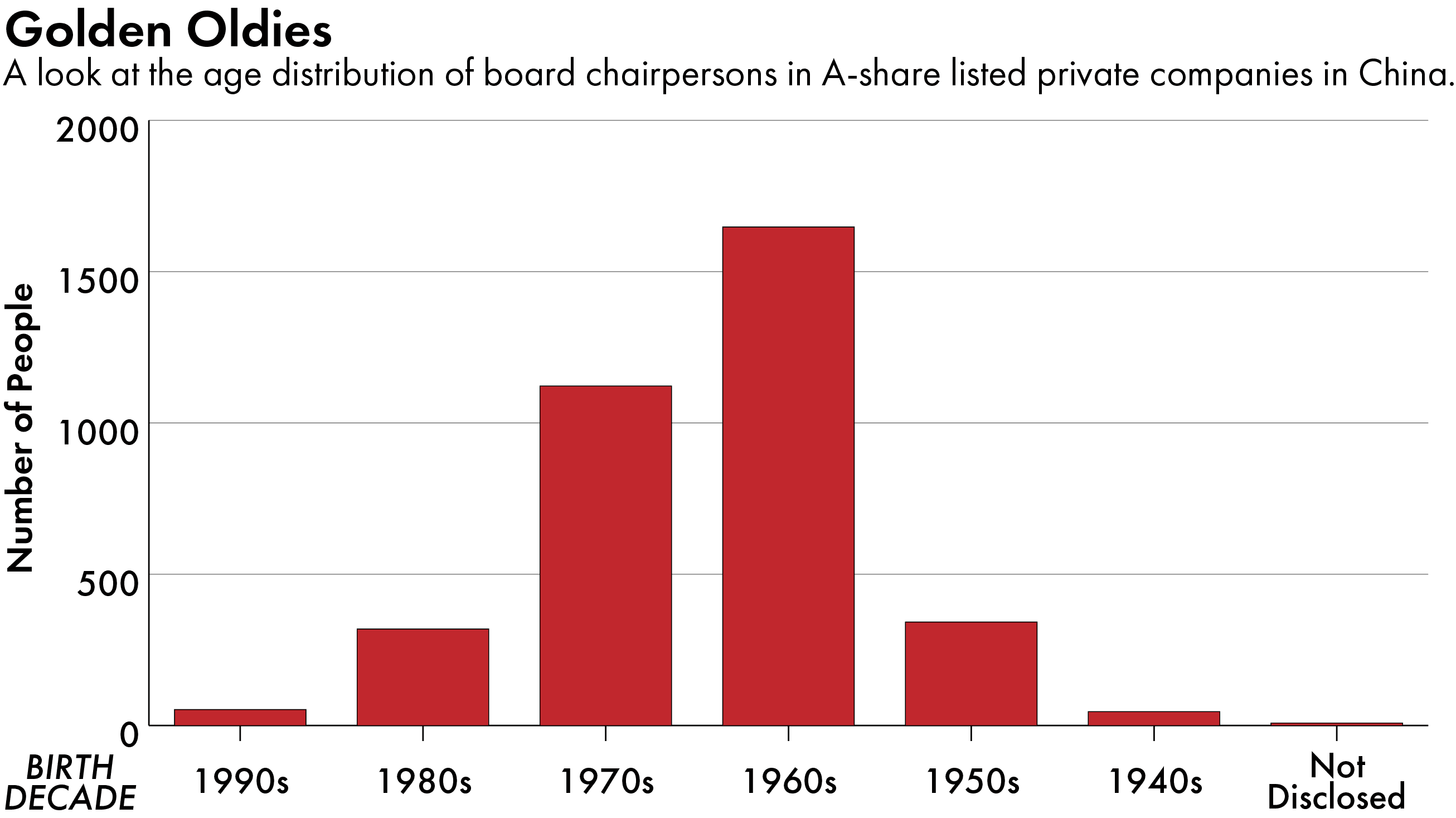

Consider privately-owned firms listed on Chinese stock exchanges. As of last April, 58 percent of their chairmen were born in the 60s or earlier, which put them above the age of 65, according to data from the financial terminal iFinD. Only 28 percent of family businesses in mainland China are managed by second generation successors, much lower than the global average of 40 percent, according to a 2022 report by KPMG.

While business succession usually takes place in waves in more developed economies, a vast transfer of company ownership in China is occurring within a relatively narrow period of time. As Fan Xinyu, a scholar at the Cheung Kong Graduate School of Business has observed, this is largely because of the country’s short history of privatization.

As a result, the passing of the corporate torch in China is an urgent matter with far-reaching consequences for the broader economy. And there are many factors unique to the country that complicate the process.

For one, the decades-long one child policy meant that many Chinese tycoons only have a single child who may, or may not, want to inherit the business.

They also do less planning than their international counterparts when it comes to succession. According to a recent survey by HSBC, 27 percent of Chinese entrepreneurs are looking to exit their businesses within the next five years, but nearly 60 per cent have no succession plan in place, the third highest rate after Taiwan and Hong Kong.

“Many of them may not have prepared their children to become a leader, and not just individually, but also in terms of governance or the layout and structure of the company,” says Kevin Au, director of the Centre for Family Business at Chinese University of Hong Kong.

This has, in some cases, made it more difficult for heirs apparent to fill their parent’s shoes. One example is Kelly Zong Fuli, the 43-year-old daughter of the late billionaire Zong Qinghou, who founded Wahaha Group, one of China’s largest beverage companies. Despite her involvement in the company’s management for over two decades, shareholders and government officials challenged her leadership following his death last February, which led to her resignation.

To her credit, Ms Zong did not quit. The plot thickened when she eventually negotiated her way back to the helm, but the shakeup was an example of the power struggles that can ensue in the absence of advance planning.

In other cases, there has been conflict between founders and their heirs, who have different upbringings and thus different expectations and values. “The older generations grew up during very tough times,” says Rui, of CEIBS. “But the young generations are raised in a very comfortable environment, so they don’t have the chance to prove themselves.”

Second-generation entrepreneurs have advantages of their own, of course. By one estimate, up to 80 percent are educated abroad. And many bring their own set of skills to the table — be it international exposure and digital savviness — and can help their family businesses digitize, expand overseas or modernize their management structures.

But these efforts by heirs to prove their worth ultimately hinge on their ability to win the trust of their parents and other veteran executives who helped build the company from scratch.

Kuang Hong returned to join his family business after studying in Australia. He took up the baton at Xingyi, a firm in Wuxi, Jiangsu that produces environmental protection equipment, in 2018. He recalls clashing with his father and facing pushback from workers who questioned his authority during the early years.

The older generations grew up during very tough times. But the young generations are raised in a very comfortable environment, so they don’t have the chance to prove themselves.

Oliver Rui, co-director of the Centre for Family Heritage at the China Europe International Business School in Shanghai

“It was difficult to implement my ideas, unless there was sufficient evidence and a strong argument to prove my direction was correct and convince my father and his peers,” he recently told China Entrepreneur.

Even with his father’s support, Kuang estimated that only 20 percent of his plans to improve safety and governance were executed. He had a say in the operations only after he helped the company enter new foreign markets, which now account for 60 percent of its sales.

It was a similar situation for Zhang Zhuotian, heiress of Putian Integrated Housing, a Zhejiang company that makes modular homes. The 28-year-old was at loggerheads with her father over her plan to adopt an intelligent customer relationship management system. She wanted to improve efficiency; her father didn’t see the need for change.

“Our negotiations fell apart. At one point, we were only communicating through emails. He didn’t approve [the plan] until I wrote him a 3,000-word essay,” she said at a conference in December. The digital system would later enable the company to seal its biggest deal of all time — a 130 million yuan ($18 million) order to supply container homes for the World Cup in Qatar in 2022.

Joseph Fan, a professor at the University of Queensland, studied over 200 Chinese-run firms in Hong Kong, Taiwan and Singapore in 2015. He found that they lost, on average, 60 percent of their value after the founders stepped down. This happened, he believed, in part because intangible assets, such as relationships and trust with key stakeholders, are difficult to pass on. But some external factors are also to blame.

For one, macroeconomic conditions today are grim. The next generation of entrepreneurs is taking over at a time when China’s age of easy growth is over and the private sector is in retreat in a range of industries. The average return on equity of private enterprises listed in China — a metric for their profitability — has been decreasing in the years before their transfer of power and the decline continued after, according to a 2022 report by Soochow Securities, a Shanghai brokerage firm, which analyzed firms that passed on the batons between 2010 and 2021.

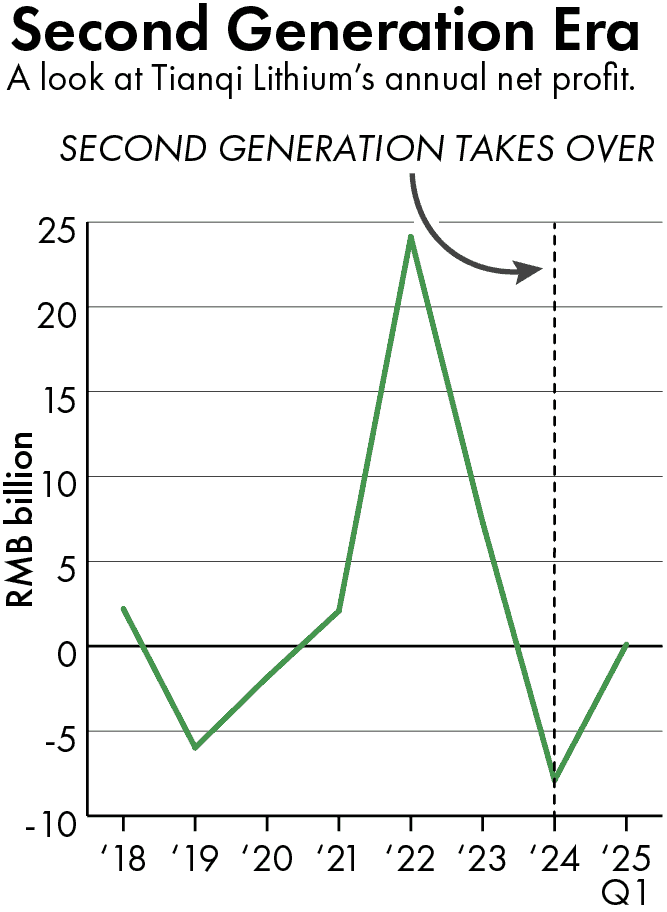

Tianqi Lithium, a leading lithium producer based in Sichuan, posted a loss of 7.9 billion yuan ($1.1 billion) last year, after 38-year-old Jiang Anqi replaced her father as the company’s chairman last April.

The elder Jiang defended his daughter during an earnings call in March, attributing the loss to challenges in the wider industry and describing it as a “good experience” for the management team.

If their children cannot step up, entrepreneurs have the option of appointing professional managers; putting the companies up for sale; or, worse, shutting the business. Tsinghua University’s Research Center for Global Family Business estimated that some 16 million private enterprises in China could discontinue as a result of succession challenges.

Fan worries there may just not be enough new blood to revive and sustain the private sector, which remains the most dynamic part of the economy. “I’m not sure because the next five years [for the] the Chinese economy will be highly volatile and uncertain. And there are very few newcomers or existing businessmen who are willing to make investments.”

Rachel Cheung is a staff writer for The Wire China based in Hong Kong. She previously worked at VICE World News and South China Morning Post, where she won a SOPA Award for Excellence in Arts and Culture Reporting. Her work has appeared in The Washington Post, Los Angeles Times, Columbia Journalism Review and The Atlantic, among other outlets.